{kind=link}

Options to the 24.3% Gen Z gender property hole

You have most likely heard in regards to the gender pay hole and the superannuation hole, however there’s one other essential hole that always goes unnoticed: the gender property hole.

CoreLogic‘s newest Ladies and Property report sheds mild on this missed problem, revealing some putting revelations.

Initially, it could look like progress when contemplating total property possession charges: ladies barely surpass males, with a 68.7% possession charge in comparison with males’s 67.4%. Nevertheless, a better look reveals a special story, particularly amongst youthful generations.

Mortgage dealer Alex Veljancevski (pictured above) emphasised the significance of understanding these tendencies, notably when serving younger feminine purchasers.

“All brokers, no matter gender, ought to study this hole and contemplate the best way to alter our providers to higher meet our purchasers’ wants and slim the divide,” Veljancevski stated.

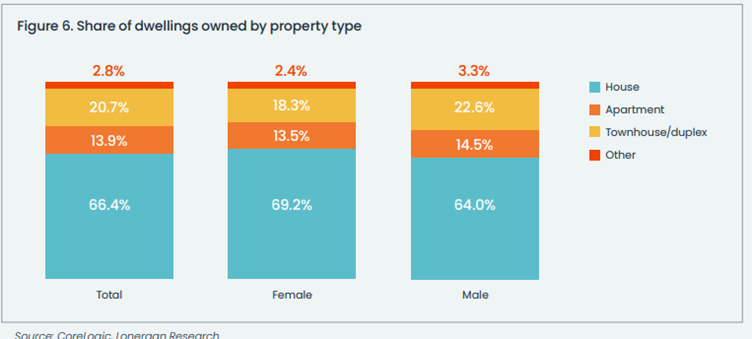

Unveiling the gender property hole

Delving deeper, CoreLogic’s analysis highlights disparities in funding patterns. Males keep the next charge of funding in residential dwellings, with 14.1% proudly owning at the least one residential funding property in comparison with 12.5% of females.

The survey additionally requested about different types of property funding, offering the examples of economic property, industrial property, or vacant land. Simply 2.2% of males reported having at the least one different type of funding property, barely increased than 1.2% of females.

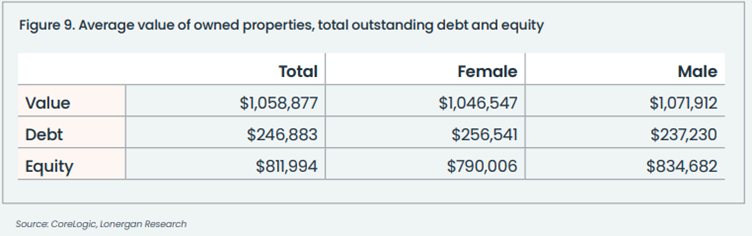

Furthermore, the report touches on the valuation and debt dynamics, revealing intriguing insights.

Regardless of ladies proudly owning the next proportion of homes, usually extra precious than items, their common reported worth is barely decrease than that of males ($1,046,547 for girls in comparison with $1,071,912 for males).

Feminine-owned property values are likely to cluster between $500,000 and $1,499,999, whereas males’s properties present a flatter distribution.

Regardless of this, ladies report barely increased common excellent debt, leading to a decrease total dwelling fairness place.

The function of joint possession

The best way ladies purchase property additionally contributes to the gender property hole.

Joint possession emerges as a prevalent avenue for girls to entry the property market, with extra ladies than males utilizing this association.

For girls on decrease revenue, this may be an efficient strategy to get onto the property ladder sooner by sharing of housing prices. Nevertheless, this has its personal complexities probably creating conditions of economic dependence and monetary abuse.

This may increasingly additionally pose some vulnerability for girls who’re single, or people who expertise a relationship breakdown.

Affordability constraints amongst Gen Z ladies

Affordability constraints considerably contribute to the gender property hole, notably amongst youthful generations. Whereas ladies might aspire to homeownership, restricted monetary sources usually pose a big barrier.

Respondents incomes lower than $100,000 yearly exhibit a house possession charge of 61.4%, in comparison with 86.6% amongst these incomes greater than $100,000.

Varied components contribute to this hole. Age performs an important function, as each dwelling possession and better incomes are usually achieved later in life. Moreover, socio-economic background influences entry to property possession, with higher-income people usually benefiting from household wealth or inheritance.

Apparently, ladies keep the next charge of property possession when revenue is taken into account. For girls incomes lower than $100,000, the possession charge was 62.1% (in comparison with 60.6% for males), rising to 91.0% for these incomes over $100,000 (83.2% for males).

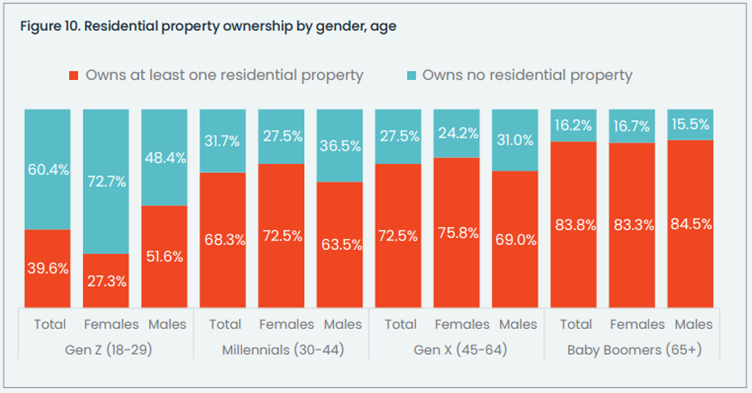

Nevertheless, the notable hole that persists amongst Gen Z respondents (51.6% of males personal a property in comparison with solely 27.3% of girls) can partly be chalked right down to variations in revenue.

Gen Z ladies, on common, have decrease incomes and are more likely to have interaction in part-time or informal employment.

This discovering is intriguing as a result of discussions about earnings for women and men usually centre on the well-documented hole ensuing from older ladies assuming unpaid parental or caregiver duties.

“Clearly, affordability constraints exacerbate the gender property hole amongst younger individuals, underscoring the necessity for focused interventions to handle this systemic problem,” Veljancevski stated.

Different causes for the gender property hole

Whereas affordability constraints play a task, they don’t absolutely clarify the hole’s persistence. Veljancevski identifies three principal components.

First, the common man earns greater than the common lady – for each $1 earned by males, 88c is earned by ladies, based on the Office Gender Equality Company.

How brokers can tackle the gender property hole

Addressing these disparities requires a multifaceted strategy.

How you can tackle the pay hole

A part of the rationale the gender pay hole exists is as a result of males usually tend to be in positions of authority than ladies.

“As a result of people usually tend to favour (usually unconsciously) individuals like them, it means, all issues being equal, that males usually tend to rent and promote males than ladies,” Veljancevski stated. “That may apply as a lot to the mortgage broking business as society generally.

“So if the business made a acutely aware effort to extend the share of feminine illustration – solely 26.9% of brokers are ladies, based on the MFAA – we’d be capable to slim the pay hole, at the least in our business.”

How you can tackle the danger tolerance hole

“Brokers – particularly male brokers – have to recognise that the common lady requires extra reassurance round shopping for property and taking up debt than the common man,” stated Veljancevski.

“Which means we now have to supply the common feminine consumer with extra schooling.”

How you can tackle the monetary literacy hole

“We additionally have to recognise that the common lady has much less monetary literacy than the common man. Once more, that requires extra schooling – nevertheless it must be delivered in a means that feels empathetic relatively than patronising.”

The underside line

In the end, closing the gender property hole isn’t just a matter of equality; it is about empowering people to realize monetary safety and well-being.

Brokers, as key gamers within the monetary panorama, have a pivotal function in driving this transformation.

How do you service your younger feminine purchasers? Remark under.

Associated Tales

Sustain with the most recent information and occasions

Be a part of our mailing record, it’s free!