{kind=link}

If in case you have cash in any of the native 3 financial institution accounts, congratulations, now you can activate a “cash lock” function to lock up a portion of your funds in order that it can’t be transferred or withdrawn. The brand new safety transfer was formalized in December 2023 as a part of enhanced banking safety measures in Singapore, however the dangerous information is, in case you’re on DBS / UOB, you’ll have to consider whether or not you’re prepared to surrender your (increased) curiosity in change for this extra safety.

Background: enhanced safety wanted to thwart scammers

The rise in banking scams right here lately have led to many Singaporeans shedding their lifelong financial savings, or retirement funds. Final 12 months, greater than S$330 million was siphoned out of victims’ financial institution accounts right here, with Singapore victims shedding essentially the most to scammers globally. What’s extra, the profile of victims have modified as it’s not the aged who fall prey, and in accordance with the Singapore Police Pressure, younger adults are actually the almost certainly to be cheated in scams.

This has been closely mentioned in Parliament, with a helpful end result being that our 3 native banks have now moved to launch a “cash lock” function on deposits. This permits prospects to “lock up” their funds in order that they can’t be transferred out, thus safeguarding depositors’ hard-earned monies at the same time as scammers proceed to evolve their rip-off techniques to cheat extra unwitting victims.

In latest weeks, all 3 native banks have launched their “cash lock” function, though every comes with totally different executions. Probably the most important distinction maybe boils all the way down to how a lot curiosity your “locked” funds will earn – and the charges aren’t fairly for among the banks.

It’s fairly telling that in Singapore, out of the 47,000 accounts and $3.8 billion that has reportedly been locked, OCBC owns the bulk share at 33,000 accounts and $3.2 billion locked (~85%).

On this article, I dive into the variations between every financial institution’s cash lock function, and query why, by selecting to lock up our monies and defend them from scams, we customers need to forfeit (increased) rates of interest that we might in any other case earn in our default Excessive-Yield Financial savings Account.

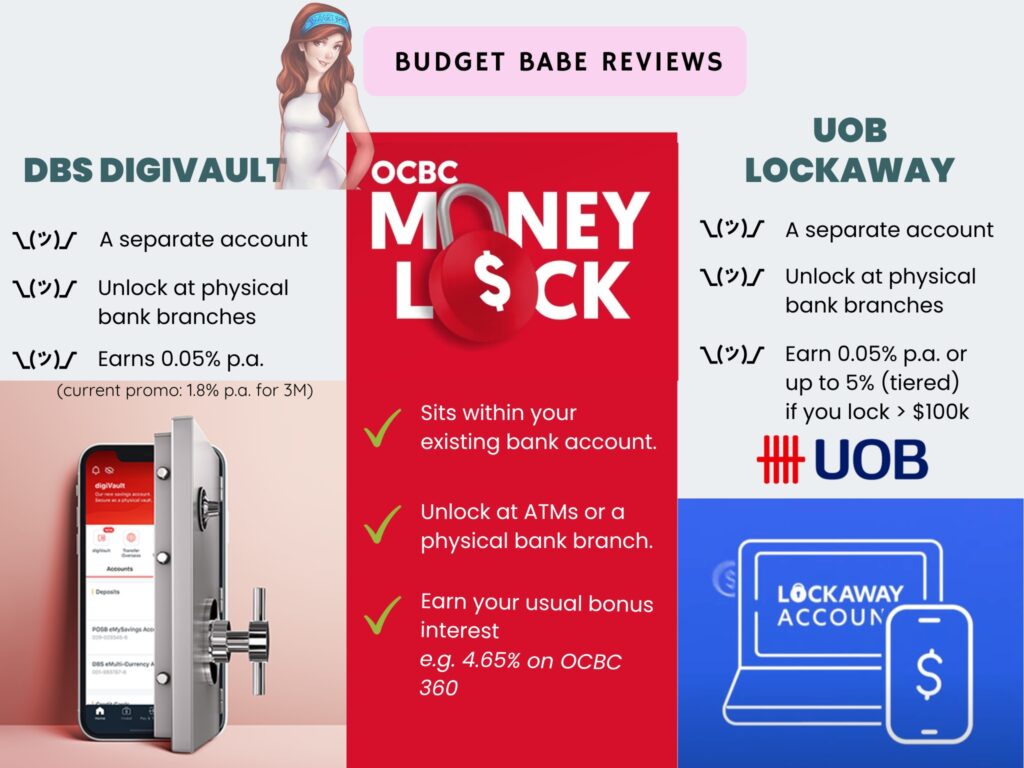

Right here’s how every of the three native banks fare:

In contrast to OCBC, the place your locked funds proceed to qualify and earn bonus curiosity, each DBS and UOB have opted for a totally totally different strategy, ensuing of their prospects having to decide on between larger safety (by locking up their funds) or increased curiosity (with out locked funds).

So earlier than you resolve to lock up your funds or which financial institution to lock it up with, please learn to grasp how every of them work, and the trade-offs concerned in every technique:

DBS digiVault

Prospects of DBS/POSB who want to lock up their funds might want to open a digiVault. Merely put, digiVault is a My Account with added safety the place deposited funds can’t be digitally transferred out.

To entry funds in your digiVault, you will have to personally go to a DBS/POSB department to boost a request and confirm your id earlier than you may “unlock” and switch funds again to your private account to liquidate them.

| The way to lock? | – Open up a digiVault and deposit your funds into the account. – Funds in digiVault can’t be digitally transferred out. |

| The way to unlock? | You have to to go to a DBS/POSB department in-person and confirm your id earlier than you’ll be allowed to “unlock” your funds and switch them again to your different DBS/POSB accounts the place they can be utilized. |

| How a lot curiosity do I earn? | 1.8% p.a. (capped at $50,000 per buyer) for 3 months so long as you open earlier than 29 February 2024.

After that, your funds will solely earn 0.05% p.a. |

You possibly can open up a number of digiVault accounts (e.g. in your financial savings vs. your fastened deposits). Nevertheless, solely the primary digiVault account will probably be eligible for the bonus extra curiosity.

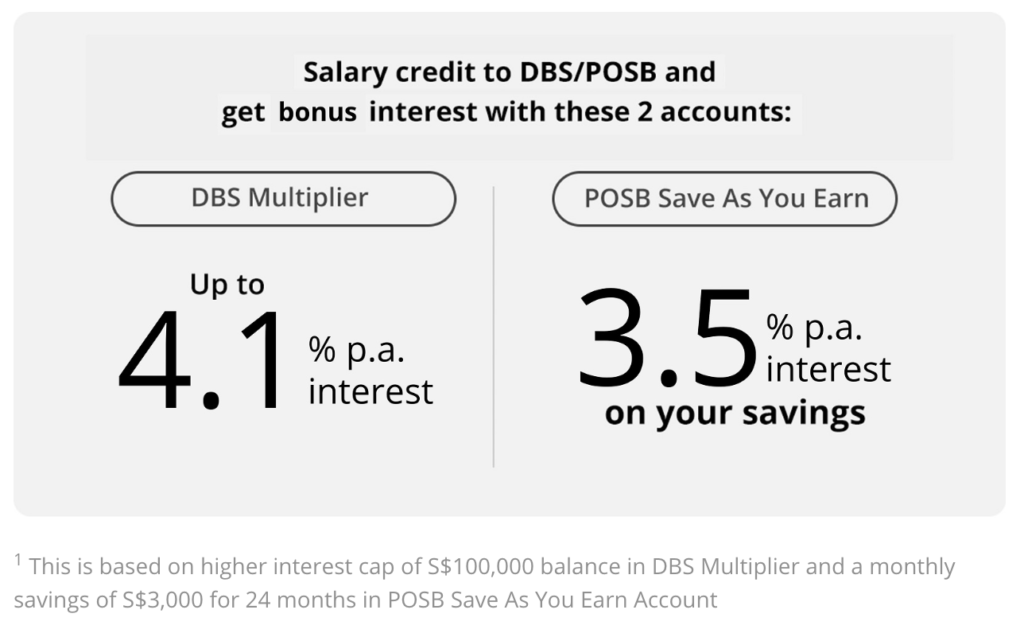

The 1.8% p.a. curiosity appears to be like good on paper – till you understand that this lasts just for 3 months and that this drops again to the usual 0.05% p.a afterwards (since that is technically a DBS My Account). Distinction this to what you may be getting in case you stored your funds in your DBS Multiplier and/or POSB SAYE account as a substitute.

Lock up your funds for larger safety however accept a decrease curiosity payout, or ignore the cash lock function solely and keep on with your present DBS excessive yield financial savings account(s)? You’ll need to resolve.

OCBC Cash Lock

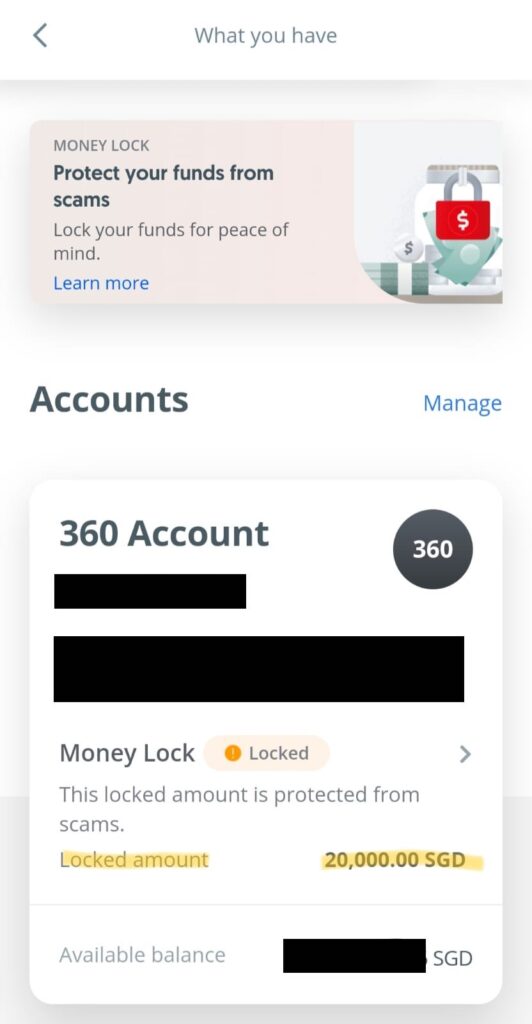

In distinction, OCBC prospects have it a lot simpler as a result of you do not want to open a brand new checking account to make use of OCBC Cash Lock, because the function is accessible to all new and present OCBC present and financial savings accounts. I merely tapped on the “Cash Lock” on my OCBC app and my funds have been locked up in underneath a minute.

Funds locked within the chosen account are aggregated with the funds that aren’t locked to calculate the curiosity to be earned. Because of this, this implies you’ll not miss out on the bonus curiosity earned in your account balances for performing on a regular basis banking transactions, particularly for these of us on the OCBC 360 Account!

| How to lock? | Faucet on “Cash Lock” and select which account funds you want to lock. |

| The way to unlock? | At any bodily OCBC ATMs (along with your card) or financial institution department. |

| How a lot curiosity do I earn? | The curiosity that you’d in any other case earn in your OCBC account e.g. 2.80% on Bonus+ or as much as 4.65% – 7.65% for OCBC 360. |

And in case you urgently want your funds, unlocking can also be a breeze as it may be finished at any OCBC ATM just by utilizing your bodily ATM debit or bank card, and your PIN. And in case you’re abroad, you may submit a request through the Secured Mailbox within the OCBC Digital app or Web Banking for a customer support consultant to contact you as a substitute.

UOB LockAway

Much like DBS, you will have to open a brand new account – UOB LockAway – and switch in your funds that you just want to lock up. Account opening can simply be finished on-line or through the UOB TMRW app, whereas unlocking the funds requires you to go all the way down to a UOB financial institution department in-person along with your NRIC or passport. UOB won’t be issuing any debit card or ATM playing cards for UOB LockAway accounts.

| The way to lock? | – Open a UOB LockAway account on-line or at their department. – Switch in your funds to be locked. |

| The way to unlock? | You have to to go to a UOB department in-person and confirm your id earlier than you’ll be allowed to “unlock” your funds and switch them again to your different financial institution accounts the place they can be utilized. |

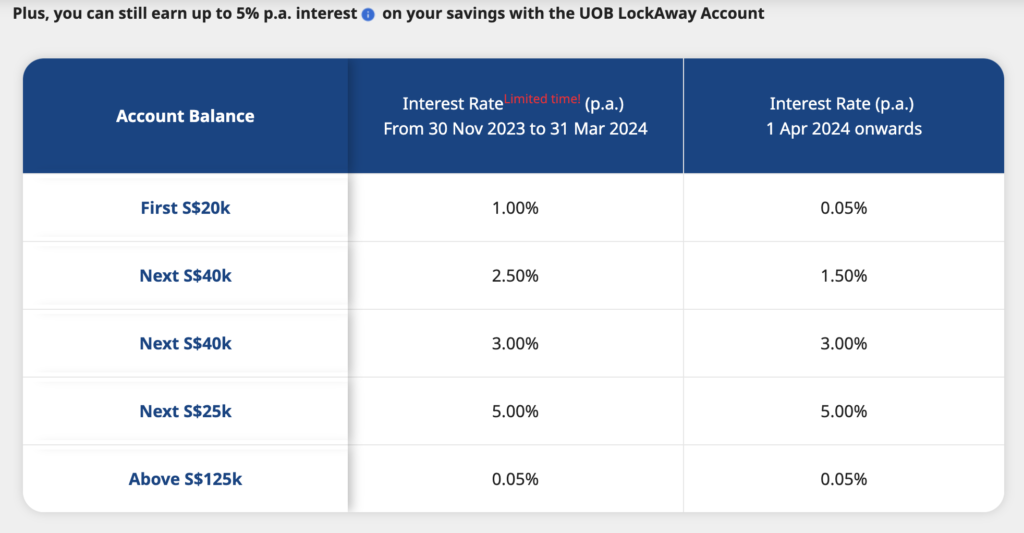

| How a lot curiosity do I earn? | 0.05% – 5% p.a. (tiered), relying on how a lot funds you lock. |

UOB advertises their charges as “as much as 5% p.a.”, however that’s largely boosted by the continuing promotional rate of interest, which ends on 31 March. Thereafter, your first $20,000 locked earns you solely a mere 0.05% p.a. And even in case you have been to lock up a sizeable sum (greater than $125k), the utmost Efficient Curiosity Fee (EIR) on the LockAway Account continues to be solely 2.45% p.a. for deposits of S$125,000 (from 1 April 2024 onwards):

The Funds Babe take:

Why ought to prospects be made to decide on between locked safety vs. increased curiosity?

Whereas I can perceive that from a business standpoint, this may seem to be an opportune second for the banks to have an excuse to pay us decrease rates of interest in change for larger “locked” safety…however that doesn’t imply I prefer it. It could be higher for the banks, however much less so for us customers.

Since OCBC can pull it off, I actually don’t see why DBS and UOB couldn’t do the identical and permit prospects to lock their funds whereas persevering with to take pleasure in their bonus rates of interest.

Why can’t DBS/POSB prospects lock their funds and proceed to earn the (increased) rate of interest from their DBS Multiplier or POSB SAYE accounts? Why can’t UOB prospects proceed to earn their UOB One’s bonus curiosity of three.85% – 7.8% p.a., whereas locking up their funds locked from scammers on the similar time?

Should we actually select one over the opposite?

Personally, I refuse to accept decrease rates of interest as a client – so it’s in all probability an excellent factor I’ve the entire above-listed Excessive Yield Financial savings Accounts, making it straightforward for me to lock my funds up with OCBC for the next causes:

- It’s tremendous fuss-free (I actually don’t wish to need to handle and take care of yet one more checking account)

- I can nonetheless take pleasure in my excessive curiosity on my OCBC 360 account.

- I can simply “unlock” my funds at any ATM with out having to waste time queuing up in-person at a financial institution department, if I wanted to.

With the Financial Authority of Singapore (MAS) now working with different main retail banks to introduce the cash lock function as nicely, I can solely hope that the opposite banks will take a leaf out of OCBC’s books and roll it out in such a means in order that their prospects would not have to decide on between sustaining their increased curiosity vs. locking up for larger safety.

But when they don’t…nicely, at the very least there’s nonetheless OCBC we are able to use.

With love,

Funds Babe